Attorneys Don’t Have a

Tax Prep Problem.

They Have a

Tax Strategy Problem.

Entity structure

•

Owner compensation

•

Estimated taxes

•

Retirement planning

•

QBI strategy

Entity structure • Owner compensation • Estimated taxes • Retirement planning • QBI strategy

If you’re an attorney or law firm owner

making strong income

but still feel like taxes are reactive,

we help you plan earlier, reduce surprises, save on taxes,

and make smarter tax decisions throughout the year.

For Attorneys and Law Firm Owners Who Want Proactive Tax Planning; Not Just a Return Prepared After the Fact.

Why Taxes Still Feel Frustrating

Even When Your Income is Strong:

Surprise

Balances Due

You find out what happened after the year is already over.

Reactive CPA

conversations

You hear advice after the window to act has closed.

Quarterly

Estimate Stress

You’re guessing instead of planning.

Owner

Compensation

Uncertainty

Salary, draws, and distributions are not tied to a strategy.

No Clear

Reserve System

You know taxes are coming, but not how much to set aside.

You Should Be

Further Ahead

High income does not automatically create financial clarity.

If taxes keep feeling rushed, painful, or harder than they should be, the issue is usually not compliance. It’s strategy.

You Don’t Need More Tax Season Surprises.

You Need a CPA Who Helps You Think Ahead.

The Issue Isn’t the Return.

It’s What Happened Before the Return:

Most attorneys have

been trained to think

about taxes at filing time.

But real tax strategy

happens earlier.

Meet:

Mark Kasminoff, CPA, J.D.

Mark has over 25 years of experience working in the accounting and tax field, and has built an excellent reputation for quality service and personal attention.

He has a Bachelor’s Degree in Accounting from the University of Nevada Las Vegas, is Certified as a Public Accountant, and earned his Juris Doctor Degree from William S. Boyd School of Law in May 2020.

You're Handing the IRS $13,400 Every Year

That You Don't Legally Owe.¹

Most solo attorneys file as sole proprietors and pay self-employment tax on every dollar they earn.

There's a simple, legal fix; the only reason most attorneys aren't using it is because

nobody told them before April.

Case Study: Solo Attorney S-Corp Tax Savings

2026 illustration · $280,000 total income · $120,000 S-corp salary · $160,000 distributions

Social Security: $184,500 × 12.4% = $22,878

Medicare: $280,000 × 2.9% = $8,120

Additional Medicare: ($280,000 - $200,000) × 0.9% = $720

Total: $22,878 + $8,120 + $720 = $31,718

Social Security: $120,000 × 12.4% = $14,880

Medicare: $120,000 × 2.9% = $3,480

Additional Medicare: $0 because the W-2 salary is below $200,000

Total: $14,880 + $3,480 = $18,360

¹This is based off the provided example case study. Individual savings may very.

Your CPA said you're over the limit.

They weren't wrong.

They just stopped too soon.

A 20% tax deduction exists for law firm owners, but it phases out at higher income.²

Most CPAs see that and move on.

A proactive advisor models what it takes to get back into range before December 31.

One retirement contribution can pays for itself in federal tax savings.²

That contribution pays for itself.

Case Study: Law Firm Owner QBI Planning

2026 illustration · $420,000 taxable income before QBI deduction · Married filing jointly · Pass-through legal practice

Excess over threshold: $420,000 - $403,500 = $16,500

Phase-out percentage: $16,500 / $150,000 = 11%

Eligible SSTB percentage: 100% - 11% = 89%

QBI deduction: $420,000 × 20% × 89% = $74,760

Target taxable income: $403,500

Taxable-income cap: $403,500 × 20% = $80,700

Additional QBI deduction: $80,700 - $74,760 = $5,940

Tax value depends on final bracket and full return facts.

²This is based off the provided example case study. Individual savings may very.

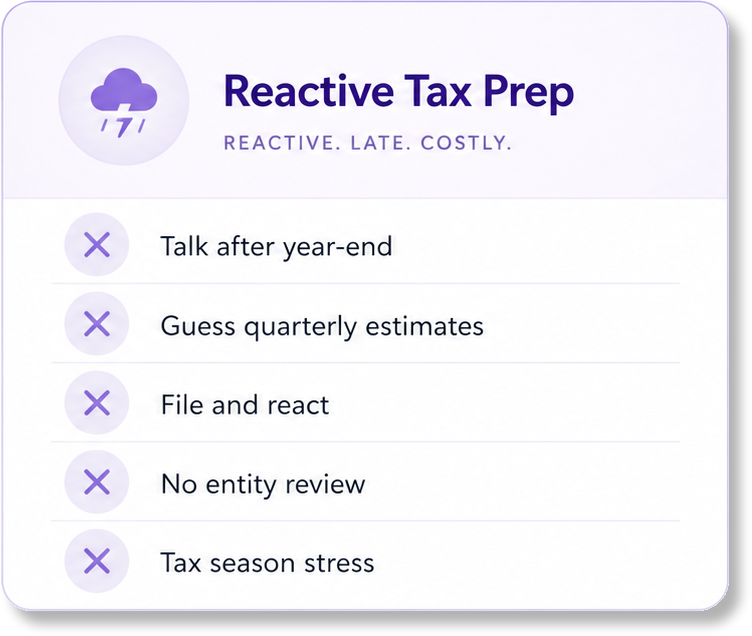

Reactive vs Strategic Tax Prep:

Who’s This For:

If you’re only looking for the cheapest once-a-year return preparation, this is probably not the right fit.

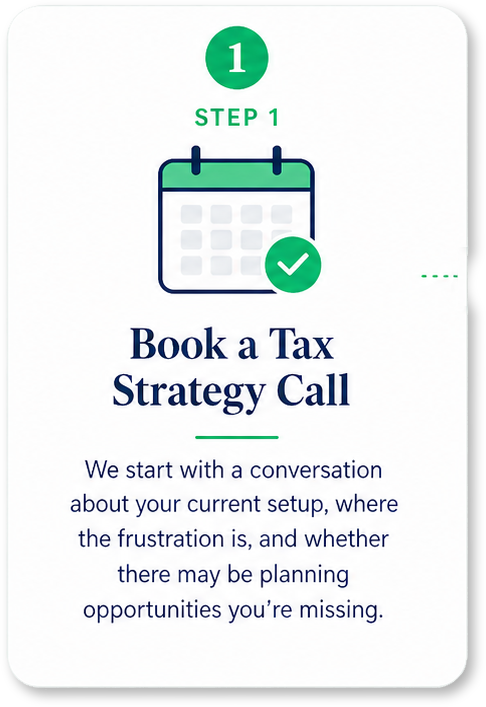

How the Process Works:

We Are Not Built Around Once-a-Year Tax Prep.

With Mark’s 25+ years of experience and a proactive tax advisory team, attorneys choose us because we help them think ahead; not just react at filing time.

What We Do Differently:

For many attorneys, that is the difference between simply getting returns filed and actually having a tax strategy.

Why Attorneys Choose a Strategic Approach:

Attorneys are used to thinking in terms of structure, risk, timing, and documentation.

Taxes should be approached the same way.

The difference is not just filing the return. It’s making the right decisions while they still matter.

That shift is often what makes taxes finally feel manageable.

Frequently Asked Questions:

For this page and process, yes.

This service is designed specifically for attorneys and law firm owners, with planning tailored to legal practices and high-income attorney households.

No.

The focus is proactive tax planning and advisory support during the year, not just preparing returns after year-end.

That’s common.

Many attorneys already have a CPA. The key question is whether proactive planning is happening early enough and often enough to improve outcomes.

That’s exactly what the initial call is for.

We can quickly determine whether your situation is a one-time issue or something that would benefit from ongoing planning support.

Attorneys and law firm owners with solid income, growing complexity, and a desire for more proactive tax planning are usually the best fit.